![]()

|

WATSON-WYATT HAS DOCUMENTED THE

RELATION BETWEEN HOW COMPANIES MANAGE TALENT AND SHAREHOLDER VALUE. The enclosed report comes

to us from Watson Wyatt (www.watsonwyatt.com). BOARD OPTIONS, INC. Boston, MA “Helping Companies Manage

the Senior Executive Assignment CycleÔ Can the way a company

manages its human capital significantly affect its financial performance? Yet a crucial question

remained: Do better people management strategies actually create higher

market value? Or do financially successful companies simply have more

resources to allocate to human capital initiatives? We now have powerful

insight into the answer. Our second Human Capital Index study allowed us to

compare one set of companies at two points in time to analyze the

correlation. The results are in and they are dramatic. Superior human capital

practices are not only correlated with financial returns they are, in fact, a

leading indicator of increased shareholder value. Further, we found that

superior HR management leads financial performance to a much greater extent

than financial outcomes lead good HR. We were also able to identify certain

HR practices as value drivers and throw a cautionary flag in front of some

conventional practices actually associated with a decrease in financial

performance. The results of this study

are more meaningful now than ever before. While the state of the economy is

largely uncertain, demographic trends are not. There is no doubt that the

labor shortage will continue well into the next decade and that superior HR

practices are a key to attraction, retention and more and more, business

outcomes. It is also a certainty that executives will now, more than ever,

look to HR to justify expenditures and demonstrate the economic value of an

organization’s people practices. The overriding message:

If a company’s goal is to improve shareholder value, a key priority must be

its approach to human capital. In the first HCI study,

conducted in 1999, Watson Wyatt surveyed more than 400 U.S. and Canada-based

companies that were publicly traded, had at least three years of shareholder

returns, and a minimum of $100 million in revenue or market value. We asked a

wide range of questions about how the organizations carried out their human

resources practices, including pay, people development, communications and

staffing. Responses were matched to

objective financial measures, including market value, three- and five-year

total returns to shareholders (TRS), and Tobin’s Q, an economist’s ratio that

measures an organization’s ability to create value beyond its physical

assets. Publicly available data from Standard and Poor’s Compustat database

were used to access the financial information needed. To investigate the

relationship between human capital practices and value creation, a series of

multiple regression analyses were conducted, identifying a clear relationship

between the effectiveness of a company’s human capital practices and

shareholder value creation. Thirty key HR practices were associated with a 30

percent increase in market value. Summary HCI scores were created for

individual organizations so that results could be expressed on a scale of 0

to 100. An HCI score of 0 represents the poorest human capital management,

while a score of 100 is ideal. In 2000, a European HCI

survey was conducted to gain a more global perspective on these issues. More

than 250 responses from 16 countries were received. The survey included 200

questions in six languages and covered companies of all sizes and from all

sectors of the economy — more than a third of participants were in the Euro

500 and more than a quarter were in the Global 500. The findings from the

European study were similar to the North American results, with improvements

in 19 key HR practices associated with a 26 percent increase in market value.

In early 2001, the HCI

research was conducted again, this time including responses from more than

500 North American companies. In this most recent research, the participants

reflected a broader view of business and included some larger, more prominent

firms — with average annual sales of $4.68 billion, $8.45 billion in market

value and 18,697 employees on average. Fifty-one of these companies

participated in both the 1999 and 2001 surveys. The European and new

North American data were then merged. The result is a complete respondent

base of more than 750 companies in the United States, Canada and Europe with

at least three years of shareholder returns, 1,000 or more employees and a

minimum of $100 million in revenues or market value. Results Link Superior

Human Capital Practices to Higher Shareholder Return The results from the 2001

HCI study are just as definitive as those from 1999: The higher a company’s HCI

score, the higher its shareholder value. In other words, the better an

organization is doing in managing its human capital, the better its returns

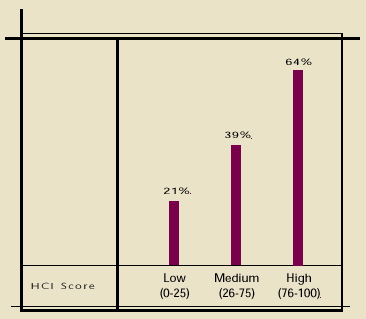

for shareholders. We broke the companies into three groups based on their

summary HCI scores. Those in the low group averaged a 21 percent five-year

return. The medium group averaged 39 percent. Those with high HCI scores

returned 64 percent over five years (Figure 1). Figure 1: Five-Year Total Returns to

Shareholders In addition to providing

dramatic evidence that good human capital management matters, the HCI study

shows precisely which HR practices — amid the ever-increasing portfolio of

options — have an impact on the bottom line. This year’s study identifies the

49 specific HR practices that play the greatest role in creating shareholder

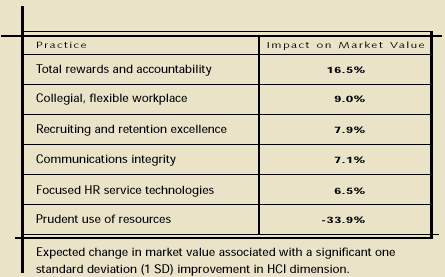

value. We have divided those practices into six dimensions (Figure 2). The

research quantifies exactly how much an improvement in each practice could be

expected to increase a company’s market value. For example, a company that

makes a significant improvement * in all of the practices categorized under

“Total Rewards and Accountability” should see its value improve by 16.5

percent (Figure 2). And a significant improvement in 43 key HR practices is

associated with an increase of 47 percent in market value. Additionally, one

dimension, "Prudent Use of Resources" indentifies six practices

that diminish shareholder value. Figure 2: Key Links Between Human Capital * What constitutes a

“significant improvement”? A one standard deviation increase. Most answers to

HCI questions are on a 1 – 5 scale, so a significant change is a

one-scale-point movement from a 1 to a 2, a 2 to a 3, and so on. The first HCI study

confirmed that there was a positive relationship between the quality of a

company’s HR practices and its economic results. But it did not offer

resolution to the debate that has raged for years: Do effective HR practices

drive positive financial results or do positive financial results lead to

better HR practices? Two years ago, we noted

that the best performing companies did not simply have better-funded

programs, they had entirely different programs than the poorly performing

companies. The high performers employed certain programs (e.g., broad-based

stock options) that low performers did not. They stayed away from certain

programs (e.g., training employees for future jobs) that low performers

embraced. If it were true that good financial performance simply afforded

rich companies the ability to implement elaborate HR programs, one would

expect to see the same types of programs across the board. We did not. Yet it

was still not proof that superior HR management was causing high market

value. The best we could offer at the time was that the relationship probably

moved both ways. But our latest study

yields the missing crucial data. Fifty-one companies participated in both the

original and the follow-up HCI studies. We have HCI scores and financial

performance information for 1999 and 2001. To see which way the

relationship truly runs, we simply compared two different correlations:

If better financial

performance is what creates superior HR practices, Correlation B should be

larger. If, in fact, the way companies manage their human capital is what

drives financial success, Correlation A should be larger. Our results were

dramatic. Correlation A, .41, is statistically significantly larger than

Correlation B, .19. The cross-lag panel analysis demonstrates HR practices

are not only associated with business outcomes, but also create them. Moreover,

a careful inspection of all the data shows that for every available

correlation calculated over time, the relationship between past HR practices

and future financial performance is stronger than the relationship between

past financial outcomes and future HR practices. We will be following this

data prospectively in longitudinal studies, but for now the weight of the

evidence clearly favors human capital practices as a leading — rather than a

lagging — indicator of business success. Figure 3: Correlation Analysis There’s no question that

it pays to manage people right. Organizations have long

focused resources on other aspects of their companies, including

infrastructure, R&D, sales and advertising, just to name a few. These

things can increase shareholder value creation in measurable ways. Some — but

certainly not all — tried to use their human capital to increase returns to

shareholders. But even these companies were taking a shot in the dark,

because no one could quantify which human capital programs were linked to

good outcomes. The business case has

been building and Watson Wyatt’s Human Capital Index research makes it

airtight. The linkage between superior human capital management and superior

shareholder returns has been proven. Moreover, proof that superior HR

practices drive financial results more than superior financial results drive

HR practices supports our theory: If you hire the right people, create an

environment that supports creative thinking and increased productivity,

leveraged by technology, you’ll reap the rewards. |